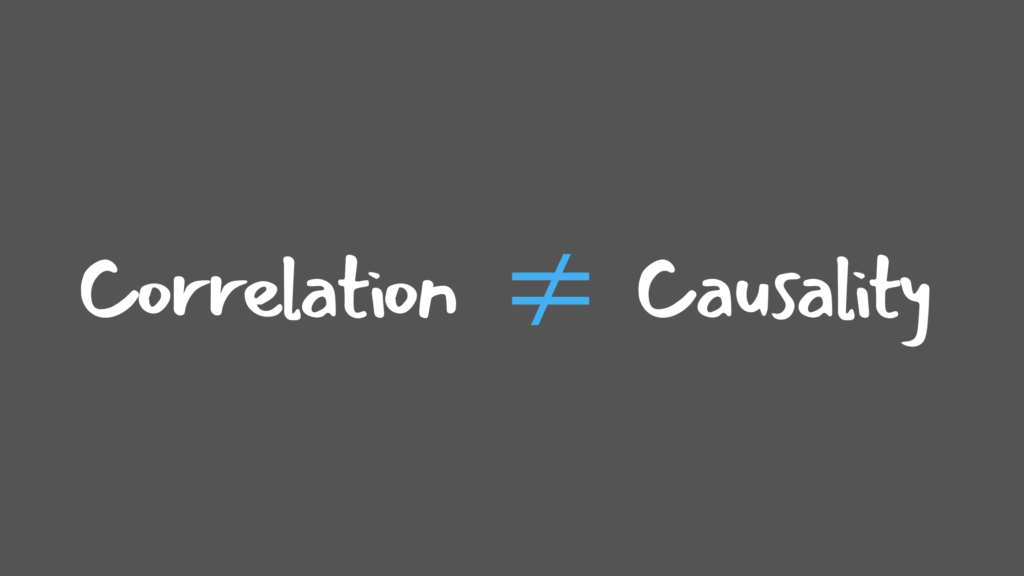

Causality is not assumed in elite finance publishing—it is engineered.

I. The Problem: When Strong Data Meets a Weak Causal Defence

The manuscript at the center of this success story was built on a rich, well-constructed dataset and addressed a question of clear relevance to financial markets. The empirical analysis produced statistically significant results, and the descriptive patterns were compelling. However, despite these strengths, the paper faced a critical vulnerability at the peer-review stage: causality was implied but not sufficiently defended.

From a reviewer’s perspective, particularly at a Tier-1 finance journal such as the European Journal of Finance, this gap is decisive. The existing empirical blueprint relied on correlations that were open to multiple interpretations. Potential reverse causality, simultaneity bias, and omitted variable concerns remained insufficiently addressed. As a result, the relationship between the key explanatory and outcome variables was exposed to reviewer attack.

In finance publishing, strong data alone is never enough. Without a hardened strategy for addressing endogeneity in finance research, even robust datasets can be judged methodologically fragile. The paper was at risk of being classified as “interesting but not causal”—a common and often fatal reviewer verdict.

II. The Audit: Diagnosing the Endogeneity Fault Lines

The first step was a structural audit of the econometric logic, not just the estimations themselves. Rather than asking whether the results were “correct,” the audit focused on a more important question: How would a skeptical reviewer try to dissect this paper?

This audit revealed that while the empirical correlations were consistent with the theoretical narrative, the manuscript did not sufficiently separate association from causation. The reviewers could plausibly argue that the explanatory variable was endogenous—driven by unobserved factors, reverse feedback loops, or simultaneous determination with the dependent variable.

At this stage, it became clear that incremental robustness checks would not be enough. What was required was a methodological reinforcement capable of isolating the causal channel explicitly. To address this, the study was re-designed to incorporate IV Probit and Two-Stage Residual Inclusion (2SRI) analyses. These techniques are particularly well-suited to nonlinear models and offer a defencible strategy for handling endogeneity without distorting the underlying research question.

This was not a cosmetic fix. It was a deliberate decision to rebuild the causal logic of the paper in a way that would withstand elite peer review.

III. The Fix: Re-Architecting the Causal Blueprint

The IV Probit and 2SRI frameworks were fully integrated into the econometric narrative.

The implementation phase focused on re-architecting both the Methodology and Results sections to make the causal defence explicit, transparent, and reviewer-proof.

First, the endogeneity problem was clearly named and motivated. Instead of burying the issue in technical footnotes, the revised manuscript openly acknowledged why simultaneity bias and reverse causation were plausible concerns in this context. This signaling alone marked a shift from a defensive to a confident scholarly posture.

Second, the IV Probit and 2SRI frameworks were fully integrated into the econometric narrative. Instrument selection was justified theoretically and empirically, first-stage relevance was discussed, and exclusion restrictions were clearly articulated. The paper no longer asked reviewers to “trust” the results—it showed precisely how the causal effect was isolated.

Third, the results section was reorganised to guide readers through the logic of causality step by step. Baseline correlations were presented as descriptive anchors, followed by the causal estimations that corrected for endogeneity. Differences between naïve and instrumented estimates were interpreted carefully, reinforcing the importance of the causal correction rather than overstating effects.

Through this process, the manuscript developed what can only be described as a hardened causal spine—one that aligned fully with the expectations of finance reviewers trained to interrogate identification strategies.

IV. The Outcome: From Vulnerable to Publication-Ready

With the endogeneity gaps closed and the causal logic fortified, the manuscript moved decisively from a vulnerable state to a publication-ready blueprint. The revised paper no longer relied on implied causality; it demonstrated it through rigorous econometric design.

More importantly, the revisions repositioned the author from a reactive respondent to a methodologically authoritative scholar. By directly addressing causality versus correlation in econometrics—and by transparently correcting for simultaneity bias—the paper met the intellectual standards expected by Tier-1 finance journals. By identifying and fixing the endogeneity fault lines early, the manuscript emerged stronger, clearer, and fully aligned with the demands of top-tier peer review.